By Shaun Strydom, CEO, Contactable

No enterprise set out to build a patchwork. They built responses, with the best tools available at the time.

Compliance needed a KYC tool. Fraud needed a fraud tool. Onboarding needed a digital journey. Each problem had its own vendor, and the point-solution era did exactly what it was meant to do: it digitised an industry that had to move at COVID speed. The vendors selling those tools couldn’t have offered anything else back then. The integrated category didn’t exist yet.

Integrated Identity Platforms emerged because the patchwork worked -until scale exposed its limits. This isn’t a story about anyone making the wrong call. It’s a story about a market that has matured around decisions made when those were the only ones available.

“Point solutions weren’t designed to fail. They were designed to solve one thing well, long before anyone needed them to talk to each other.”

Here are the numbers I think most leadership teams will find staggering:

- 48% of enterprises are using 4+ vendors in onboarding today (The Rise of Integrated Identity Platforms, Liminal, 2023, p. 11).

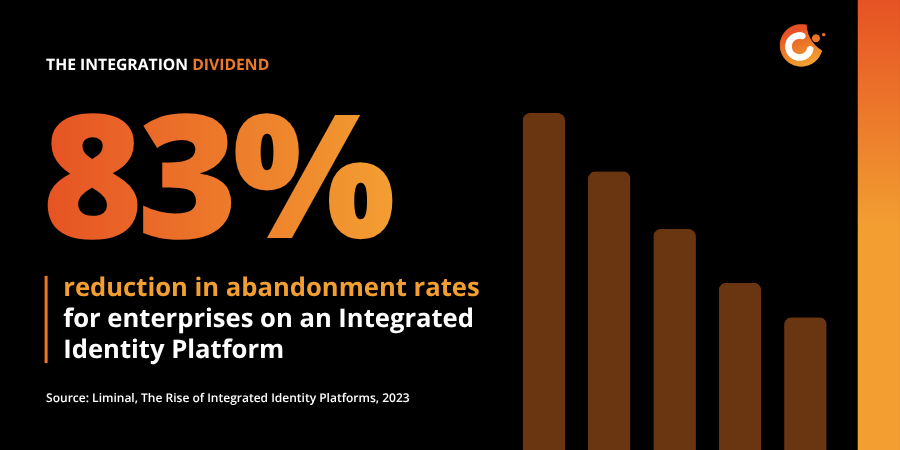

- Liminal found that enterprises using an integrated identity platform see an 83% reduction in abandonment rates — which tells you exactly what the patchwork was silently costing before (The Rise of Integrated Identity Platforms, Liminal, 2023).

- 67% of enterprises want to switch to IIPs in the next five years (The Rise of Integrated Identity Platforms, Liminal, 2023, p. 11).

- Liminal published this research in 2023 — so two of those five years are already behind us.

The visible cost is friction. The hidden cost is blindness. When your fraud engine, onboarding flow and authentication layer don’t share signals, you have decisions being made with half the picture.

That’s what a patchwork actually costs.

In Africa, the seams show faster

POPIA, KYC regulation sharper SAFPS expectations (link below). The compliance bar in this market is rising while customer patience is shortening. And every new geography means rebuilding identity logic from scratch when it lives across seven different systems.

And the threat side is getting louder. Impersonation fraud listed by the Southern African Fraud Prevention Service spiked 38% in 2024 alone (SAFPS, 2024). That isn’t a vendor problem. It’s the system being tested at a pressure no point-solution architecture was designed to absorb.

We see this everywhere we work. Telcos, automotive, financial services, you name it. Different industries, same patchwork: identity logic spread across half a dozen vendors, each solving a slice, none seeing the whole.

Strategy isn’t the problem. Implementing it is.

Most enterprises already have an identity strategy on paper. The challenge isn’t deciding what good looks like. It’s executing it across every channel, every regulatory checkbox, every market.

And in the age of the empowered digital customer, that execution is only getting harder. Customers expect frictionless. Regulators expect rigour. Boards expect both, at speed. Holding all of that together on a patchwork worked at smaller scale. At enterprise volume, across multiple markets, with shifting compliance baselines and rising fraud sophistication, it quietly becomes the thing limiting how fast the business can move.

An Integrated Identity Platform isn’t the strategy. It’s how the strategy gets delivered across the journey.

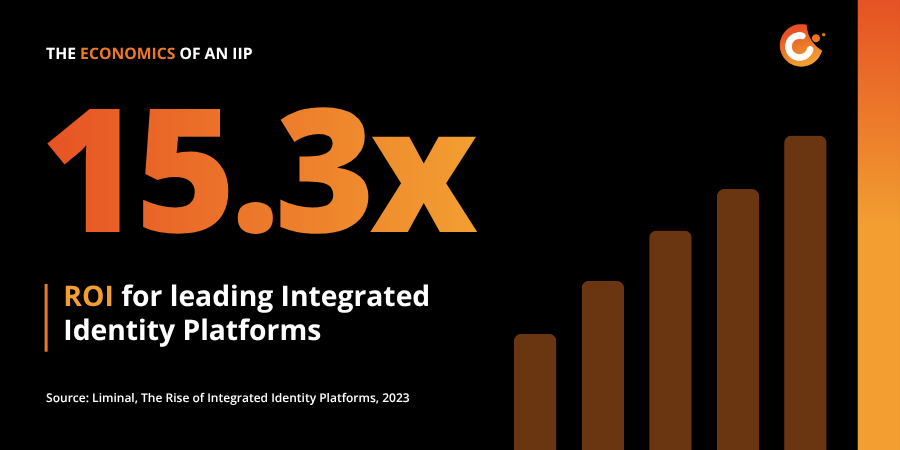

Liminal Strategy Partners — the independent firm tracking this market globally — has named Contactable the Regional Leader for Middle East & Africa in their Liminal Index for Account Opening in Financial Services. They also track the economics: a 15.3x ROI for leading Integrated Identity Platforms, through fewer abandonments, lower fraud and faster decisioning (The Rise of Integrated Identity Platforms, Liminal, 2023).

Most enterprises don’t lack an identity strategy on paper. They lack a way to execute one across the journey, at speed, without the seams showing.

The one question worth asking your CIO this week

“If our regulator audited us tomorrow, could we produce a single audit trail across identity, compliance and fraud, or would we be stitching it together from four dashboards?”

The answer tells you whether you are able to actually operationalise your strategy.

If your team is running four or more identity vendors and you’d like to compare notes, email or DM me on LinkedIn. Happy to share what we’ve learned across 15 African markets, working with telcos, automotive, financial services, you name it.

Shaun Strydom is the CEO of Contactable, Africa’s Integrated Identity Platform, named Regional Leader for Middle East & Africa by Liminal Strategy Partners. Contactable powers identity, compliance and fraud signals across the customer journey for telcos, banks and insurers in 15 African markets.

Follow us on LinkedIn | Facebook

FAQs

What’s the difference between an identity strategy and an identity stack?

A strategy is a coordinated plan for how identity supports growth across the journey: onboarding, fraud, compliance, authentication, recovery. A stack is what you end up with when each of those problems gets solved by a different vendor over time. Most enterprises think they have the first. The four dashboards they audit from tell a different story.

How many identity vendors does the average enterprise use?

Liminal’s 2024 research found 48% of enterprises run four or more vendors just for basic onboarding. At enterprise scale, the average KYC journey itself orchestrates around 10 point solutions, each one a seam to manage and audit. The cost compounds when those vendors stop sharing signals with each other.

What’s the ROI of consolidating onto an Integrated Identity Platform?

Liminal Strategy Partners measured a 15.3x return for every $1 invested in an IIP. The gains come from lower KYC abandonment, faster decisioning, lower fraud exposure, and audit-defensible logic across the journey. The longer enterprises wait, the more retrofitting the patchwork costs.

© Copyright 2012 – 2023 | All Rights Reserved | Privacy Policy | Terms of Use | PAIA Manual